Global Market Commentary

Global financial markets posted strong gains in Q3 2025, driven by robust artificial intelligence (AI) and technology demand, solid corporate earnings, and a well-anticipated Federal Reserve (Fed) rate cut. A weaker US dollar supported emerging markets. Credit, digital assets, and commodities – with notable, record-setting rallies in gold and silver – also performed well.

Equities

Global equities enjoyed a strong quarter. Growth stocks outpaced value stocks as optimism around the technology sector gathered pace. Emerging market equities outperformed their developed peers, driven largely by China, where an extension of the US–China trade truce and surging AI optimism fuelled gains.

The MSCI Asia ex-Japan Index rose 11.1%, with Chinese technology stocks leading the way. The Hang Seng Tech Index gained 22.1% for the quarter and is now up 46.0% year-to-date, supported by government backing for domestic chipmakers and rapid AI product rollouts. Taiwan, with its heavy weighting to semiconductors, posted a 14.7% gain.

Japan’s TOPIX Index rose 11.0%, aided by a weaker yen, the US–Japan trade deal that reduced tariffs on nearly all Japanese exports, and continued corporate governance reforms. The US S&P 500 gained 8.1% in Q3, underpinned by resilient earnings and a solid macro backdrop. While headline inflation ticked up to 2.9% in August, tariff passthrough effects were milder than feared. This gave the Fed scope to cut rates by 25 bps in September, its first cut of the year, with guidance for further easing ahead.

Elsewhere, UK equities advanced 6.9%, supported by overseas revenues and a weaker sterling. Continental European equities lagged, with the MSCI Europe ex-UK up just 2.8%. Germany underperformed, while France eked out gains despite political instability and fiscal uncertainty.

Fixed Income

Bond markets were volatile as investors weighed political risks and fiscal sustainability concerns. Nonetheless, global bonds finished higher, with the Bloomberg Global Aggregate Bond Index up 0.6%.

US Treasuries rallied (+1.5%) as market focus shifted from inflation risks to softer growth signals. Labour market data weakened, with monthly job gains averaging just 29,000 over the summer, and prior payroll figures revised sharply lower. These revisions underscored that the US economy has been less robust than previously thought. Credit markets were supported by tighter spreads and a weaker dollar.

Conclusion

The third quarter of 2025 highlighted the market’s delicate balance between optimism and risk. Investor enthusiasm around AI, improving trade dynamics, and anticipated monetary easing supported strong gains across equities and select credit markets. Yet, beneath the surface, softer US labour data, fiscal fragility in Europe, and the potential for renewed tariff-driven inflation present ongoing challenges. While resilience in certain areas of the economy has surprised to the upside, recession risks have risen according to our dashboard of leading indicators. We remain alert to potential downside risks.

Local Market Commentary

Economic Snapshot

South Africa’s economy grew by 0.8% in Q2 2025, up from 0.1% in Q1, but Q3 data points to a slowdown to around 0.4%, per early estimates. Yearly growth for 2025 is now forecast at 1.0%, below the 1.6% hoped for earlier. Political stability has provided some support, but high unemployment, infrastructure challenges, and global trade tensions continue to hinder growth.

Jobs and Social Strains

Unemployment hit 33.2% in Q2, with youth at 62.2%. Poverty affects 68% of people, straining the R259bn social grant. The rand averaged 17.24 to the dollar in Q3, vulnerable to China slowdowns. FDI inflows were R11.7bn in Q1 but flipped to R73.5bn outflows in Q2 on corporate restructurings like Anglo’s platinum spin-off; Q3 shows modest recovery to R8bn.

Policy and Budget

The South African Reserve Bank (SARB) may cut rates again in Q4, given subdued inflation and weak growth. The budget deficit is projected at 4.8% of GDP, and gross debt is expected to rise to 77.4% of GDP by FY2025/26.

Bonds Yields Continue to Fall

South African bonds rallied in September 2025, with 10-year yields dropping to just above 9%—lowest since mid-2021—on low inflation, high real yields and JPMorgan index changes drawing R15bn foreign inflows. This rally, which extended into early October, saw non-resident holdings more than triple from R48.5 billion at the end of Q2 to approximately R162 billion by late September.

Precious Metals Rally While SA Inc Struggles

Gold breached $4,000/oz in October 2025, up 50% YTD, driven by central bank buying, geopolitical tensions, and a weaker USD amid Fed rate cuts. JSE gold miners like Harmony Gold, AngloGold Ashanti and Gold Fields outpacing the physical metal’s rise due to their high leverage led gains. This led to the JSE resources index up 119%, contributing ~0.2% to GDP via exports. Platinum stocks also rallied, with prices hitting $1,600/oz, However, “SA Inc” stocks—retailers, property, and consumer goods sold off sharply, with the JSE General Retail Index down 8% in Q3 due to weak domestic demand and high interest rates, widening the performance gap. Gold and platinum’s high-beta outperformance masked broader market weakness, with 60% of JSE stocks posting negative returns.

Looking Ahead

Q4 could see 0.5% growth, supported by holiday spending and a continual rally in precious metals. Some market commentators have forecasted 1.6% growth for 206, contingent on trade stability and political cohesion. South Africa’s strengths, robust financial institutions and tourism remain intact, but urgent reforms in logistics, energy, and labour markets are needed to unlock sustained growth.

Platinum Insights

Talent, Choice, and Triumph Lessons for Fund Managers from boxing greats

In both the ring and the markets, talent alone isn’t enough. Choices – critical, strategic choices, define who merely competes and who ultimately triumphs.

Take Charlie Weir, the “Silver Assassin” from Kimberley. Born in 1956, Weir was a gifted athlete, charismatic and deadly in the ring, with 31 wins in 34 professional bouts. But when he faced off against Davey Moore in Johannesburg for the WBA Junior Middleweight title in 1982, and Moore in turn faced Roberto Duran a year later, the truth emerged starkly: natural ability must be paired with experience, resilience, and timely opportunity.

Duran – seemingly past his prime, written off by pundits, made the right choices, reignited his career, and recaptured his former glory with stunning talent.

The difference between Charlie Weir (or Davey Moore) and Roberto Duran wasn’t raw skill alone. It was how Duran leveraged experience, seized opportunity, adapted his preparation, and fought smartly. The fight and destruction of Davey Moore is not easy to watch!

https://www.youtube.com/watch?v=2p91eHMs-yI&t=8s

Similarly, in the investment world, the last decade presents a parallel lesson when we compare Costco and Target.

Over the past 10 years:

- Costco delivered a 749% total return, translating into an average annual return (CAGR) of nearly 23.85%.

- Target, on the other hand, returned only 57.6%, an average annual return of about 4.7%.

If you had invested $1,000 a decade ago, it would now be:

- ~$8,490 in Costco

- ~$1,576 in Target

Why such a vast difference?

Costco’s strategic model choices, like its membership-driven business, relentless focus on customer loyalty (with a 90% renewal rate), and steady execution – compounded advantage year after year.

Target, despite being a capable and prominent retailer, made less effective strategic choices: shifting consumer tastes, heavy exposure to non-essential goods, and stiffening competition left it struggling.

In investing, like boxing, raw potential must be paired with smart, timely decisions.

What this means for fund managers

As fund managers, we are continually presented with two types of “athletes” or companies:

- Some are naturally talented but vulnerable, just like a brilliant young fighter who hasn’t faced real adversity (like Charlie Weir or Davey Moore).

Others might appear beaten up, discounted, or underestimated, but if they have the right fundamentals, resilience, and a sound strategy (like Roberto Duran), they can achieve extraordinary long-term victories.

Choosing where to allocate client capital is no different from choosing which fighter to back:

- Do we buy glamour and potential?

- Or do we invest in business models that have proven endurance, loyalty, and resilience under pressure?

Costco’s story reinforces that when we choose wisely, patiently, and strategically, our clients reap the compounding rewards.

In contrast, chasing the “bright young things” without due diligence and foresight – much like placing faith in an untested fighter facing a hardened champion, can result in disappointment.

Decision-making defines outcomes

Charlie Weir and Davey Moore were great athletes. Roberto Duran was a great champion. Target was a good retailer. Costco built a great business.

As fund managers, our legacy will be determined not just by finding “good” investments, but by choosing great ones at the right time – just as Roberto Duran chose the right fight, the right preparation, and the right moment to deliver one of boxing’s greatest comebacks.

Every choice matters. And the compounding impact of those choices can be the difference between mediocrity and greatness in our clients’ portfolios.

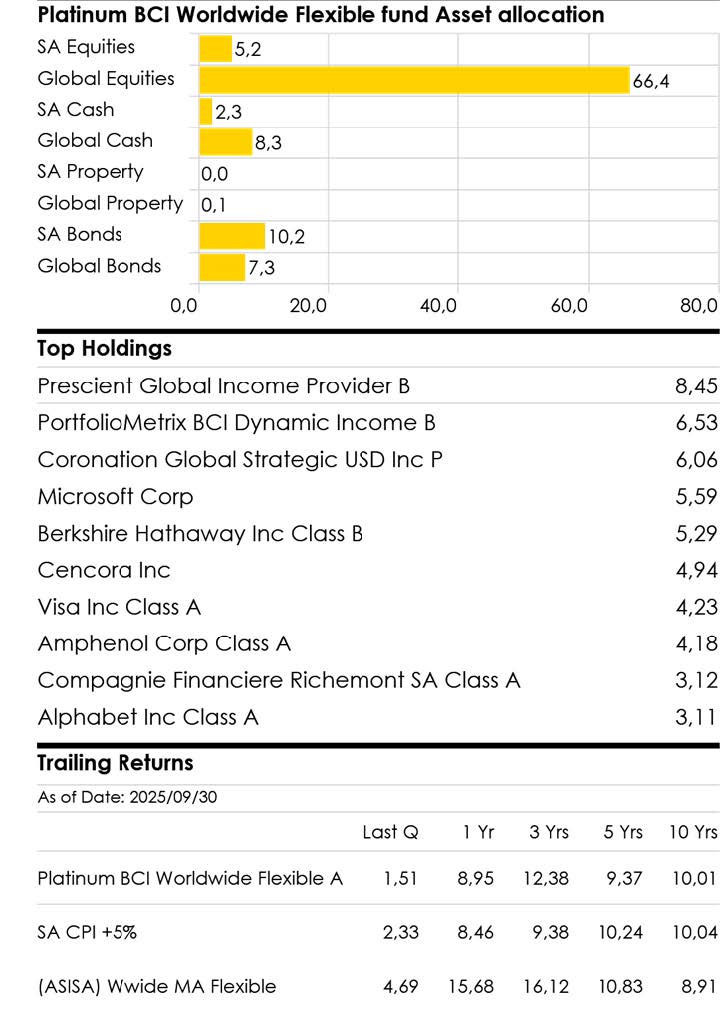

The Platinum BCI Worldwide Flexible Fund

The Platinum BCI Worldwide Flexible Fund has delivered a solid 12.83% return in USD year to date. In rand terms, the second quarter produced a 1.51% gain, even as a stronger rand reduced offshore returns. The stronger rand has detracted from the funds’ performance this year. Our defensive positioning has supported performance through volatility, and we made no changes to the portfolio during the period to our underlying shares. Equity exposure remains steady at around 71%.

Equity Highlights

During the quarter, the best performing share was Amphenol Corp +21.8% , driven by strong demand across its electronic connector and sensor businesses. Remgro had good results +4.9%, Walmart +2.6%, and Cencora +1.4%, further added to performance, reflecting their defensive qualities.

The main detractors were Philip Morris (-13.5%) and Texas In-struments (-13.4%), with Philip Morris impacted by regulatory and tariff challenges and Texas Instruments pressured by softer semiconductor demand. Stryker (-9.1%), Zoetis (-8.6%), and Visa (-6.5%) also weighed on returns.

Looking over the longer term, AbbVie, Apple, Amphenol, and Williams-Sonoma have remained strong contributors, with Amphenol standing out with a 91% return over the past year. On the other hand, Philip Morris and Texas Instruments have been weaker performers, they remain quality business with resilient global brands.

Bond Positioning

We maintained our barbell positioning to global and local bonds. On the local market , we exited our investment in the Taquanta Active Income Fund after the unexpected departure of key portfolio managers, reallocating to our existing bond strategies. The new manager Portfolio Metrix outperformed with its positioning in longer-dated South African government bonds. We are satisfied with all the other managers locally and offshore.

Looking Ahead

Global markets remain highly concentrated, with a small number of companies driving much of the performance in both the US and South Africa. Beneath the surface, conditions are more fragile. We therefore continue to position the funds defensively, focusing on high-quality multinationals with strong balance sheets and resilient earnings, with the goal of delivering consistent long-term value for our clients.

Note: Quarterly performance since inception: Highest 13.17% Lowest –6.68%. Annualised return is weighted average compound growth rate over the period measured. Actual annual figures are available to the investor on request. Source Morningstar as at 30 September 2025.

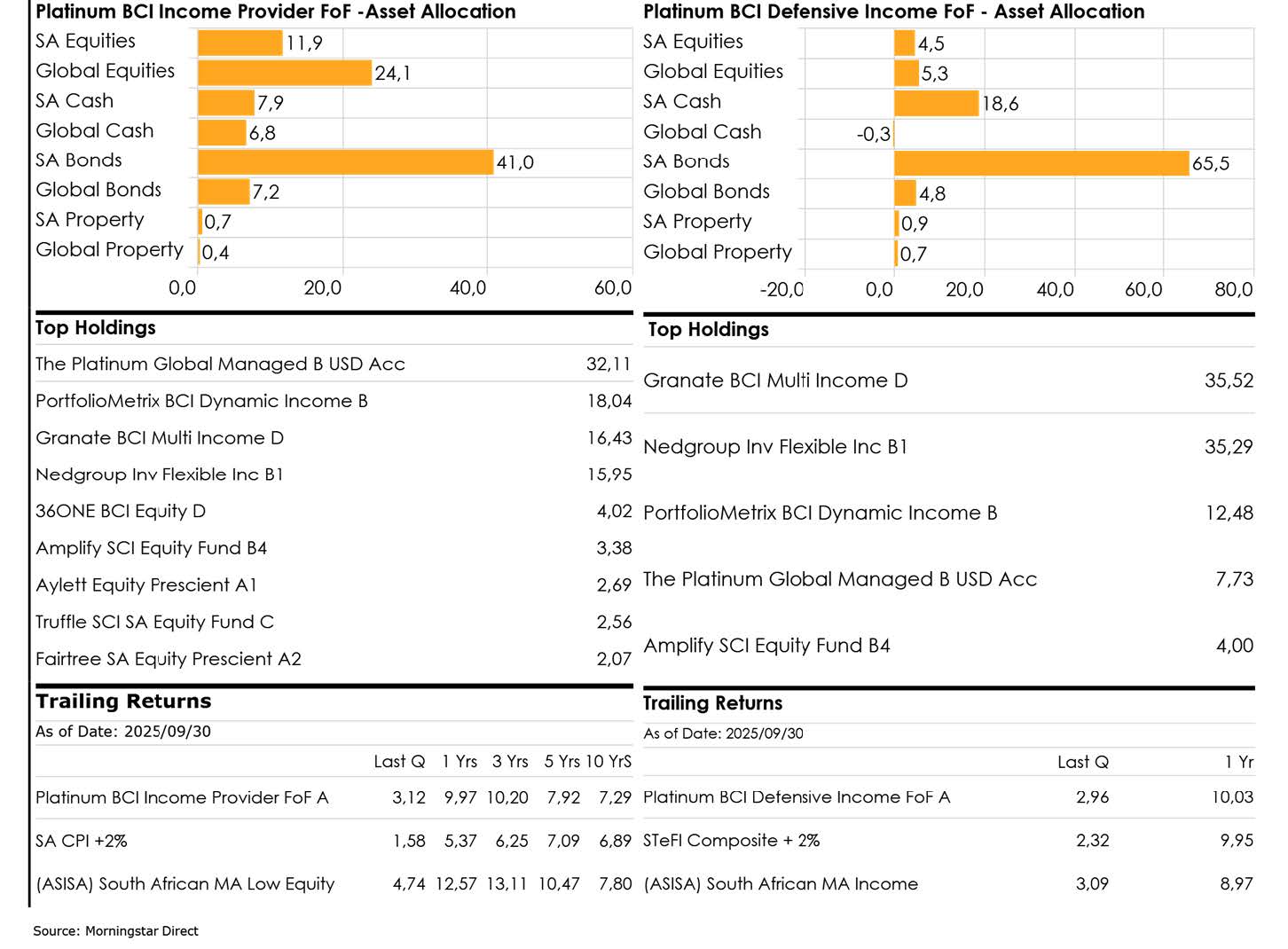

The Platinum Fund of Funds

In Q3 2025, all of the Fund of Funds outperformed their inflation or cash benchmarks:

- The Platinum BCI Balanced Plus FoF delivered a robust 5.05% return, surpassing its SA CPI+5% benchmark by 2.72%.

- The Platinum BCI Balanced FoF achieved 4.34%, exceeding SA CPI+4% by 2.26%.

- The Platinum BCI Income Provider FoF returned 3.12%, outpacing SA CPI+3% by 1.29%.

- The Platinum BCI Defensive Income FoF posted 2.96%, exceeding its STeFI Composite +2% benchmark by 0.64%.

Underlying Manager Performance

All four Fund of Funds delivered strong real returns, leveraging diversified allocations to capture market upside. Most of the local equity managers capitalised on the JSE’s rally, driven by strong performances in gold stocks and Naspers/Prosus, fuelled by a gold price and global tech sentiment. Fairtree (12.6%), Truffle (11.8%), Amplify (11.9%) and 36One (11.2%) were key contributors, leveraging these exposures effectively. Conversely, Aylett performance was lacklustre over the quarter due to its contrarian positioning, holding neither gold stocks nor Naspers/Prosus. We have scrutinized Aylett’s portfolio in depth and have engaged with this manager, confirming no signs of style drift or capitulation. We remain confident in their investment skill, expecting their disciplined approach to deliver over the long term and provide uncorrelated returns when the market cycle changes.

PortfolioMetrix, Granate, and Nedgroup all benefited from the bond rally. PortfolioMetrix’s standout performance stemmed from its tactical overweight in longer-dated South African government bonds, which rallied strongly as yields fell and foreign demand surged, amplifying returns relative to shorter-duration peers. Granate’s focus on high-quality, short-duration bonds delivered steady income, while Nedgroup’s diversified fixed-income strategy provided stability but trailed due to lower exposure to longer-dated bonds.

Manager Changes

Over the past quarter, we exited our holding in Taquanta across all our ZAR solutions. The experience and skillset of the individuals managing the Taquanta Active Income Fund were significant factors in our decision to invest in this fund. Over the past few weeks, there have been sudden departures of key investment personnel at Taquanta. After reviewing the situation, we decided to exit the investment immediately and allocate to our remaining bond strategies.

In the Defensive Income FoF, we replaced 36One with Amplify (Oystercatcher) as the equity manager. This move aims to lower the offshore currency impact and thus the overall volatility of the strategy, while providing the fund with more consistent returns.

Note: Quarterly performance since inception: Platinum BCI Balanced fund: Highest 8.62% Lowest –3.90%. Platinum BCI Income Provider fund: Highest 5.28% Lowest –1.84%. Annualised return is weighted average compound growth rate over the period measured. Actual annual figures are available to the investor on request. Source Morningstar as at 30 September 2025.

Note: Quarterly performance since inception: Platinum BCI Balanced fund: Highest 8.62% Lowest –3.90%. Platinum BCI Income Provider fund: Highest 5.28% Lowest –1.84%. Annualised return is weighted average compound growth rate over the period measured. Actual annual figures are available to the investor on request. Source Morningstar as at 30 September 2025.

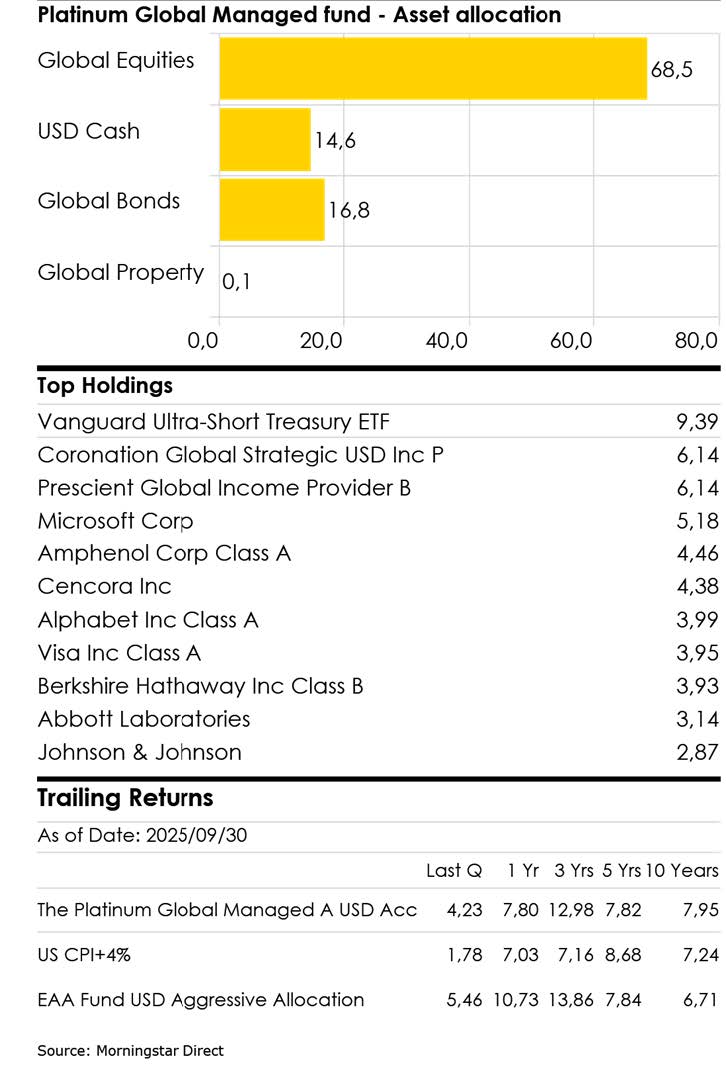

The Platinum Global Managed fund USD

The Platinum Global Managed fund delivered a return of 4.23% for the quarter, outperforming its benchmark of USD CPI+4 which was up 1.84%.

The third quarter of 2025 saw positive returns across most major asset classes as trade tensions subsided, AI euphoria continued, and expectations for near-term rate cuts from the Federal Reserve (the Fed) ramped up.

The standout performers in our portfolio were AbbVie, Apple, Amphenol Corp and Williams-Sonoma. Amphenol Corp has delivered a return of 91.42% for the last 12 months. Amphenol is a leading global manufacturer of electronic connectors, sensors, and interconnect systems used across industries from automotive and aerospace to mobile devices and broadband. Its diversified end markets, strong customer relationships, and consistent innovation have made it a resilient and high-quality compounder.

The detractors to our performance were Colgate-Palmolive Co, Philip Morris International and Texas Instruments. Colgate-Palmolive has underperformed over the past year as higher input costs and tariffs pressured operating margins, particularly in emerging markets where currency headwinds also weighed on results. Despite these short-term challenges, the company remains a quality stock, supported by its strong global brands, resilient demand in oral and personal care, and ongoing pricing power.

Our unwavering commitment remains anchored in sound fundamental analysis of the companies within our portfolio. Our companies, however, continue to deliver positive earnings results overall — a validation of our quality-focused approach and reinforcing our confidence in the portfolio. We remain happy with our holdings.

We maintain a conservative position with just over 68% in equities. Our cash balance continues to reflect our view on the state of the global economy. Holding cash helps us stabilise volatility in the fund and achieve the risk profile that best suits our private client base. Importantly, we are fully driven by our mandate — we are not trying to compete with equity funds but remain focused on delivering the best possible returns within our defined risk framework and ultimately outperform our US CPI+4 benchmark.

The prevailing market uncertainties and the subtle signs of slowing economic growth reinforce our prudent approach. Our dedication to delivering superior risk-adjusted returns over the long term remains steadfast, ensuring the best outcomes for our valued investors.

Note: Quarterly performance since inception: Highest: 16.11% Lowest: -8.98%. Annualised return is weighted average com-pound growth rate over the period measured. All performance figures quoted are sourced from Morningstar. Period ending 30 September 2025.

Company in Focus: Alphabet

![]()

Evolving Beyond Search

Alphabet, the parent company of Google, YouTube, Android and Google Cloud, is quietly transforming itself from an ad-driven internet company into a full-stack AI and technology platform. From designing its own computer chips to powering the next wave of AI and driverless cars, Alphabet is building the foundation for long-term growth.

Waymo – Driverless Cars on the Road

Waymo, Alphabet’s autonomous-driving division, has now completed over 100 million driverless miles and offers hundreds of thousands of fully autonomous rides each week across several U.S. cities. Each ride helps improve safety, reduce costs and refine the technology turning what was once a research project into a scalable, software-based mobility business.

Custom Chips – Powering Google’s AI Advantage

Alphabet designs many of its own computer chips, giving it a cost and performance edge. Its TPU chips are built specifically for AI, while its Axion CPUs power Google Cloud’s everyday computing. This vertical integration means Google’s platforms — Search, YouTube, Gemini and Workspace — run faster and more efficiently. Clients using Google Cloud benefit too, with lower costs and quicker AI performance.

Quantum Computing – Early but Promising

Alphabet’s new Willow quantum chip marks progress toward real-world applications. The first breakthroughs are likely in chemistry and materials science, such as developing better batteries or new medicines. If successful, Google Cloud could one day offer unique, premium capabilities in this emerging field.

Clean Energy – Fuelling AI Growth Sustainably

Running massive AI data centres requires reliable power. Alphabet aims to operate on 24/7 carbon-free energy by 2030. A recent agreement with NV Energy and Fervo will deliver 115 MW of around-the-clock geothermal power, helping to secure stable, clean energy, a crucial advantage as power constraints become a bottleneck for AI growth.

Practical AI – Tools for Everyday Use

Alphabet is embedding AI into the tools people already use. NotebookLM, for example, helps users summarise documents, create study guides or generate reports, while Gemini enhances Search and Workspace. These everyday AI applications increase user engagement and strengthen Google’s ecosystem of over one billion users.

Why We Own Alphabet

We like businesses that control their destiny on cost, have multiple paths to win and can self-fund ambition. Alphabet ticks all three.

They are shipping real driverless service with Waymo, running on their own silicon, securing firm clean energy for the AI era and embedding practical AI tools like NotebookLM into daily workflows. With massive cash flow, very low debt and ample room to keep investing in R&D and acquisitions, we believe their integrated innovation engine can compound value for many years. That is why we hold Alphabet in the portfolio.