Market Commentary

Global Markets: Second Quarter 2026 Review

Looking Beyond the Headlines

The second quarter of 2026 demonstrated once again why successful long-term investing requires investors to look beyond the headlines. Markets were confronted with heightened geopolitical tensions, sharp swings in oil prices and continued uncertainty over the outlook for inflation and interest rates. Yet despite these challenges, global equity markets delivered another strong quarter, supported by resilient economic growth and, most importantly, robust corporate earnings.

Markets Focus on Fundamentals

Perhaps the most interesting feature of the quarter was the contrast between market headlines and investor behaviour. While news coverage focused on conflict in the Middle East and concerns over energy supplies, financial markets quickly looked through the uncertainty. Oil prices spiked during the quarter as fears of supply disruptions intensified, only to retreat sharply as those concerns eased. Rather than reacting to short-term events, investors increasingly focused on the underlying strength of businesses and their ability to continue growing earnings.

Credit Markets: Calm on the Surface, Cracks Beneath

One of the more interesting developments during the quarter was the growing divergence between public and private credit markets. On the surface, credit markets remained remarkably calm, with investment-grade credit spreads still close to historically tight levels, reflecting continued confidence in large corporate balance sheets. Beneath the surface, however, signs of stress began to emerge. The rapid growth of private credit over recent years has resulted in greater exposure to more highly leveraged and less liquid borrowers, and during the quarter investors began to see isolated signs of strain. High-profile managers, including Blue Owl, experienced increased redemption requests in certain private credit vehicles, while concerns around valuations and liquidity continued to build across parts of the sector. Although these developments are not yet indicative of a broad credit event, they suggest that the credit cycle may be beginning to turn. We continue to monitor credit markets closely, as periods of exceptionally tight credit spreads have historically provided little margin for error when economic conditions weaken.

Currencies, Inflation and Interest Rates

The US dollar traded in a broad range during the quarter. It benefited from periods of safe-haven demand during heightened geopolitical tensions but surrendered some of those gains as market sentiment improved. The Japanese yen remained relatively weak despite the Bank of Japan’s gradual move away from ultra-loose monetary policy, as interest rate differentials continued to favour the US dollar.

Interest rates remained a key focus for investors. While inflation continued its gradual moderation across many developed economies, central banks remained cautious in signalling the timing of future rate cuts. Labour markets remained resilient, economic activity continued to exceed expectations in many regions, and policy-makers were reluctant to ease monetary policy prematurely. As a result, bond yields remained elevated and financial conditions relatively tight.

Company Earnings Remain the Key Driver

The most encouraging development during the quarter was another exceptionally strong corporate earnings season. The majority of high-quality businesses either met or exceeded market expectations, supported by healthy consumer demand, ongoing productivity improvements and continued investment in artificial intelligence and digital infrastructure. Earnings growth remained the primary driver of equity market returns, reinforcing our long-held belief that, over the long term, company fundamentals ultimately determine investment performance.

Looking Ahead

The second quarter once again demonstrated that quality businesses can continue to create value even in an environment characterised by geopolitical uncertainty, elevated interest rates and inflationary pressures. While short-term market volatility is likely to remain a feature of the investment landscape, strong earnings, resilient corporate balance sheets and disciplined capital allocation continue to provide a solid foundation for long-term investors. At Platinum, we remain focused on investing in high-quality companies with durable competitive advantages, confident that earnings growth and business quality remain the most reliable drivers of long-term wealth creation.

South African Economy: Second Quarter 2026 Review

Q1 2026 ended in crisis mode, with the Iran-Israel war triggering a sharp market sell-off and derailing what had been a promising start to the year. Q2 proved less dramatic but no less consequential — a hike, an upgrade, a ceasefire, and a gold correction all landed within a matter of weeks, while a fresh political flashpoint emerged in the background.

Rates, Ratings and a Fragile Ceasefire

The SARB raised the repo rate 25 basis points to 7.00% on 28 May — its first hike since 2023 — as oil-linked inflation from the ongoing Middle East conflict pushed April CPI to 4.0%. The MPC vote was split four-two, and the Bank lifted its 2026 inflation forecast to 4.4%. Just over a week later, Fitch delivered the other side of the story: an upgrade of South Africa’s sovereign rating to BB from BB-, its first in roughly 21 years, on the back of fiscal discipline and reform progress. A 60-day ceasefire reopening the Strait of Hormuz in mid-June then eased the energy-price pressure that had driven the hike in the first place. Between the upgrade and the ceasefire, SA bonds rallied — the All Bond Index returned close to 7.9% for the quarter — and the rand recovered from around R17.20/USD at end-March to roughly R16.40 by quarter-end.

Gold’s Reversal

Precious metals told a very different story. Gold fell from January’s record high above $5,400/oz to below $4,000/oz by late June, as a stronger-than-expected US jobs report extinguished Fed rate-cut hopes and the dollar firmed. This hit SA’s resources-heavy equity market: the JSE Allshare Index was down roughly 2.2% for the quarter, with gold and PGM-heavy counters bearing the brunt.

Political Risk Resurfaces

The Phala Phala saga returned to the fore. Following a Constitutional Court order, an Impeachment Committee was convened, and President Ramaphosa responded with an urgent High Court interdict application to halt proceedings pending a separate review of the underlying panel report. The interdict is set to be heard on 15–16 July, with the review itself only heard in September. GNU cohesion, and market sentiment more broadly, will be sensitive to how this unfolds.

Outlook

The SARB’s next decision on 23 July is finely balanced between the disinflationary relief of a firmer rand and cheaper fuel, and the upside risks the Bank explicitly flagged in May — a resumed conflict, El Niño-related drought, and non-linear second-round effects. Gold’s path depends largely on the Fed’s own trajectory under new leadership. Domestically, the impeachment interdict ruling is the most immediate political risk to watch, with implications for coalition stability extending well beyond the courtroom. South Africa’s fundamentals — fiscal discipline, a fresh ratings upgrade, six consecutive quarters of GDP growth — remain genuinely improved. Whether that translates into a calmer H2 depends on forces largely outside the country’s control.

Our Insights: Ownership Mindset

Thinking Like an Owner

There has seldom been a day in more than two decades of building Platinum Portfolios when the business has been far from my mind. Sometimes it’s a better process. Sometimes it’s a client conversation. Sometimes it’s simply asking, “How can we be better tomorrow than we are today?”

Some people might call that an inability to switch off. I see it differently. I see it as ownership.

Ownership isn’t something you do between nine and five. It’s a way of thinking. When you genuinely care about something you’ve built, you’re constantly looking for ways to strengthen it. Not because you have to, but because you want to leave it better than you found it.

The Connection Between Business and Investing

The longer I’ve spent building a business and managing investments, the more convinced I’ve become that they are driven by exactly the same principles.

At Platinum, we don’t invest as traders-we invest as owners.

That means looking beyond the next quarter or the latest market headline. Instead, we ask a much simpler question: Would we be comfortable owning this business for many years?

We’re attracted to quality businesses with durable competitive advantages, exceptional management teams, high returns on capital and resilient business models. Businesses that we believe can continue creating value long after today’s market trends have come and gone.

It’s a philosophy inspired by investors such as Warren Buffett and Charlie Munger, who encouraged us to think like business owners rather than speculators. That mindset has shaped not only how we invest, but also how we’ve built our own business.

The Quiet Power of Compounding

One of the biggest misconceptions about success is that it comes from one defining breakthrough. In reality, lasting success is usually built through hundreds of small improvements made consistently over time.

A better process.

A wiser investment decision.

Hiring someone who strengthens the team.

A more meaningful conversation with a client.

On their own, these decisions may seem insignificant. Together, they compound. Just as investment returns compound over time, so do good decisions.

Avoiding the Big Mistakes

Charlie Munger often reminded investors that success isn’t only about making brilliant decisions. It’s also about avoiding the mistakes that can permanently set you back.

That lesson has had a profound influence on the way I think.

In investing, protecting capital and managing downside risk are just as important as generating returns. The same principle applies in business. Often, long-term success comes not from doing extraordinary things, but from consistently avoiding unforced errors.

The Ownership Mindset

Perhaps that’s why owners never really stop thinking about their businesses. Not because they’re anxious, but because they care.

Whether you’re building a business, managing investments or developing your career, the principle is the same: think like an owner.

Stay patient. Stay disciplined. Keep improving.

Because lasting success is rarely created by one brilliant moment. It’s built one good decision at a time, repeated consistently over many years.

By Charolyn Pedlar, Co-Founder, Platinum Portfolios

The Platinum Funds

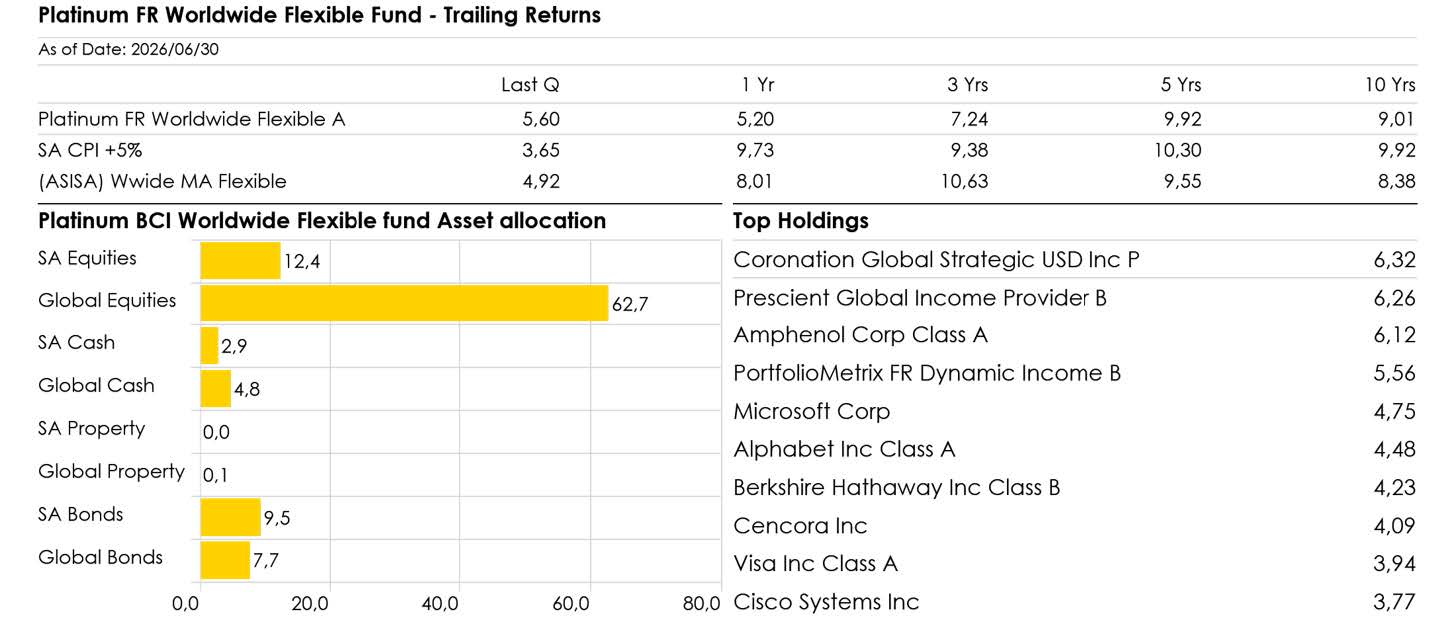

The Platinum BCI Worldwide Flexible Fund

Global markets

Two things shaped the quarter: the winding down of the conflict between the United States and Iran, and renewed excitement about artificial intelligence (AI). As peace talks progressed and it became likely the Strait of Hormuz would reopen, the oil price fell 38% from its April peak of around USD 120 a barrel. Markets breathed a sigh of relief. Developed market shares gained 13.9% over the quarter, US shares added 15% on strong company results and news that the big technology firms plan to spend close to USD 700 billion on AI infrastructure in 2026. US inflation rose to 4.2% in May, mostly because of higher fuel prices, but wage growth stayed modest at 3.5% — a sign inflation is un-likely to spiral. The Federal Reserve kept interest rates at 3.50%–3.75%. With oil now falling, we expect price pressures to ease and rates to stay on hold for the rest of the year.

South African markets and the rand

The JSE had an uneven quarter. With few large technology shares, it could not fully join the global AI rally, and weaker gold and platinum prices weighed on mining shares. Banks and property held up better, and local bonds did well as oil prices fell and global sentiment improved. Consumers remained under pressure from higher fuel costs, which kept the Reserve Bank cautious. The rand was stable against the US dollar, trading mostly between R16.20 and R16.65 and averaging around R16.50 for the quarter. A weaker dollar globally helped keep the currency steady despite the volatility in oil prices.

Fund Performance

The fund returned +5.6% for the quarter, after fees, in rands. April was strong, may saw a pullback as tensions in the Middle East peaked, and June recovered with a return of +2.0%. The fund ended the quarter with better performance and keeps its four-star Morningstar rating.

What drove returns

Technology did well. Our technology shares returned 18.8% as a group and added 4.4 percentage points to the fund’s return. The winners were the companies supplying the AI build-out: Texas Instruments (+47.8%), Cisco (+45.7%) and Amphenol (+33.8%). Alphabet (+19.1%) and Richemont (+28.4%) also did well, and our South African banks — Capitec (+16.7%), FirstRand (+12.9%) and Standard Bank (+9.0%) — benefited from a steady local backdrop. Healthcare was the main drag, falling 9.0% Zoetis was the biggest single detractor, with Cencora and Abbott also weaker. Consumer names like PepsiCo, Walmart and McDonald’s fell as higher fuel prices squeezed household spending, and Microsoft (-3.3%) lagged as investors looked for proof that AI spending is paying off.

Source: Morningstar Direct, total returns in ZAR, 1 April – 30 June 2026.

Positioning

We used the market’s strength to reduce risk slightly. Bonds and cash make up 26% of the fund, with shares at around 74%. The fund holds thirty-nine quality businesses, with the top ten making up just under half of the portfolio. Our approach remains unchanged: buy quality businesses at fair value, with a margin of safety.

Outlook

We start the second half positive on markets. The AI spending boom now needs to show real returns, and consum-ers are still feeling the effects of higher fuel prices. Encouragingly, investors are becoming more selective about which AI companies they back — an environment that suits our approach. The fund’s mix of AI beneficiaries, defen-sive quality businesses, strong local banks and a larger allocation to global income assets leaves clients well positioned.

Note: Quarterly performance since inception: Highest 13.17% Lowest –6.68%. Annualised return is weighted average compound growth rate over the period measured. Actual annual figures are available to the investor on request. Source Morningstar as at 30 June 2026.

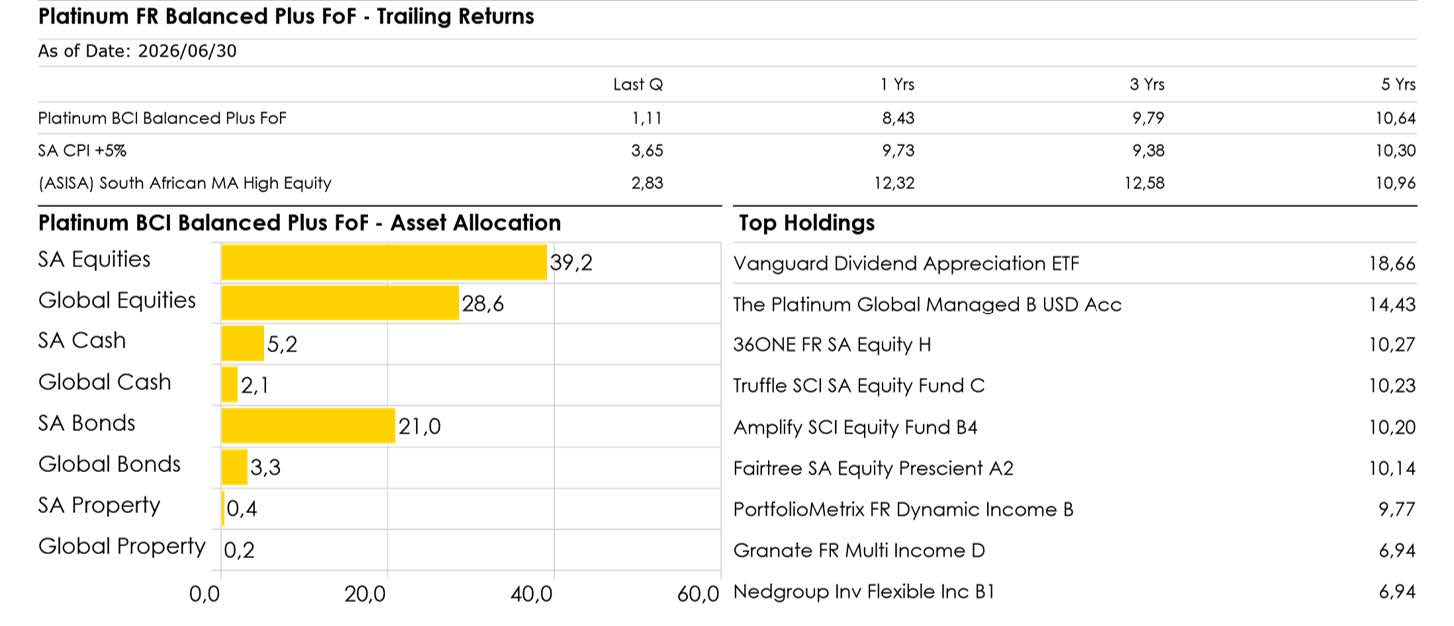

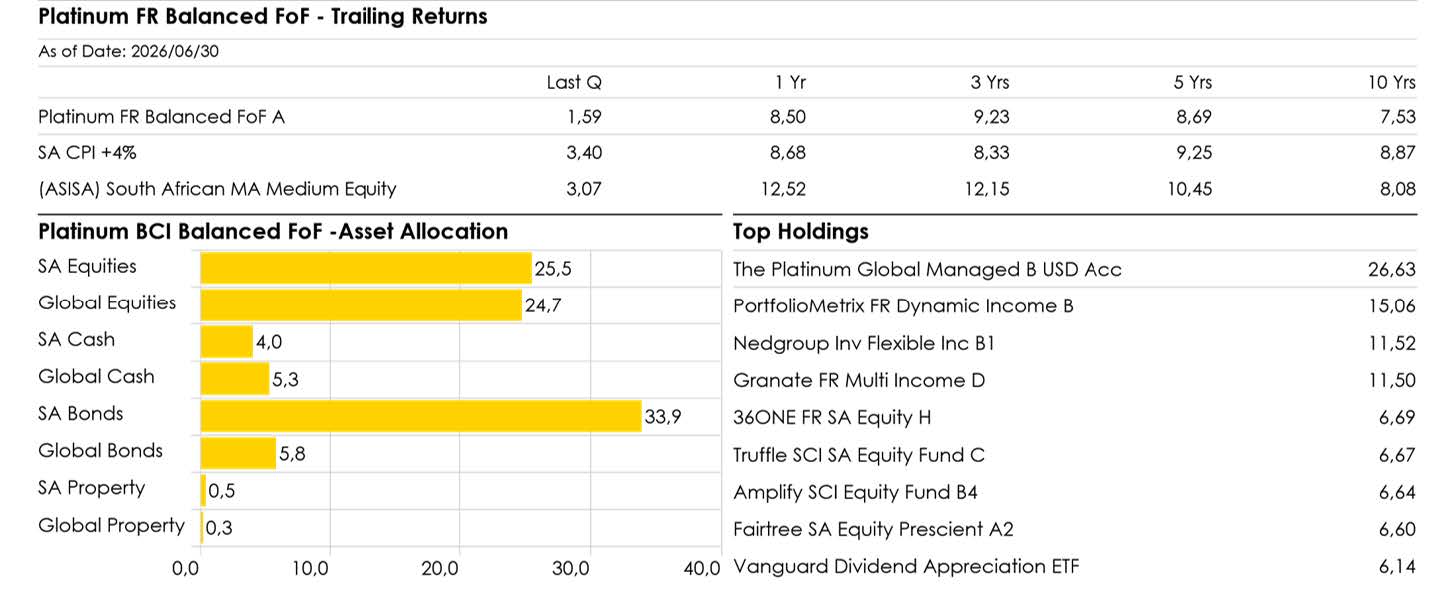

The Platinum Fund of Funds

Note: during the quarter, the Manco changed its registered name — from “BCI” to “FR” — as reflected in fund documentation and fact sheets. This is a name change only; the appointed Management Company itself has not changed, and there is no effect on the investment mandate, asset allocation approach, or the underlying managers held within each fund.

In the first quarter of 2026, only the Platinum FR Defensive Income FoF managed a positive return, as the out-break of the Iran-Israel war in late February drove sharp drawdowns across equity and bond markets. Q2 2026 told a more constructive story across the board, though the drivers shifted meaningfully mid-quarter.

- The Platinum FR Balanced Plus FoF returned +1.11% for the quarter, underperforming its SA CPI+5% bench mark by 2.54%.

- The Platinum FR Balanced FoF returned +1.59%, underperforming its SA CPI+4% benchmark by 1.81%.

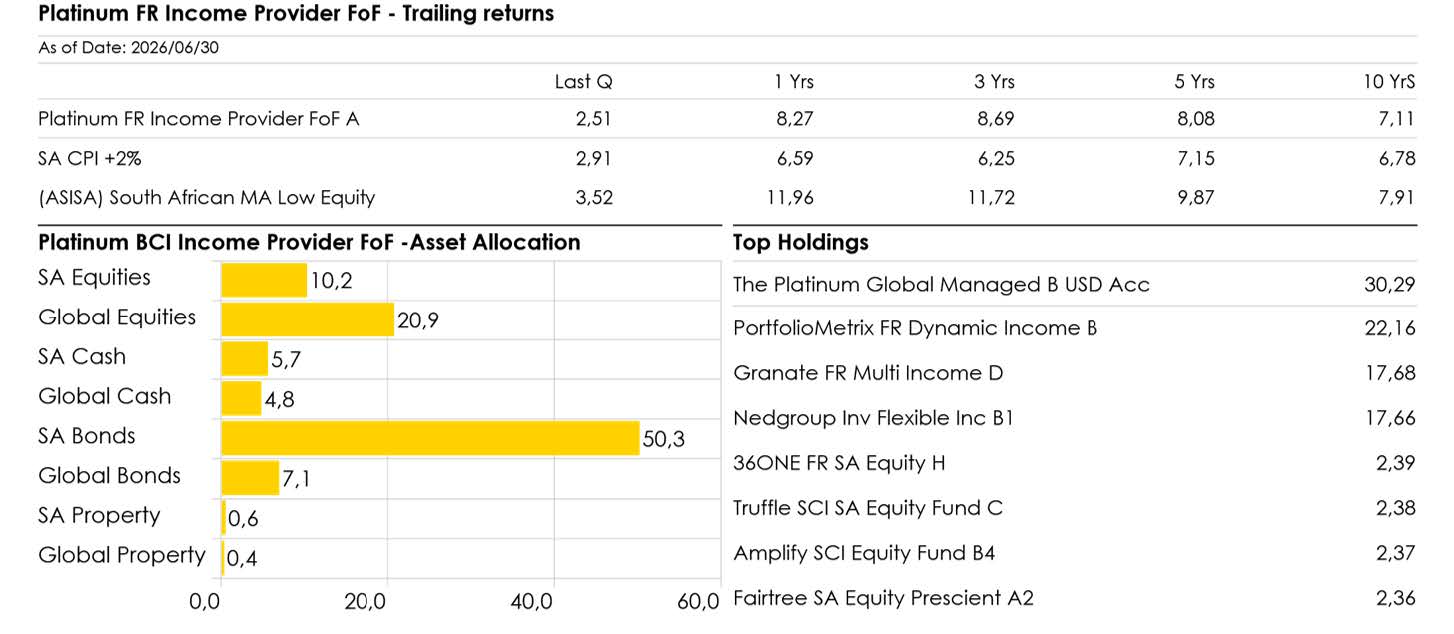

- The Platinum FR Income Provider FoF returned +2.51%, underperforming its SA CPI+2% benchmark by 0.39%.

- The Platinum FR Defensive Income FoF returned +3.50%, outperforming its STeFI Composite+2% benchmark by 1.33%.

All four funds returned to positive nominal territory this quarter, but the composition of those returns diverged sharply between equity and fixed income exposures. The SARB’s 25 basis point hike to 7% on 28 May 2026 — its first since 2023, driven by oil-linked inflation from the ongoing Iran conflict — initially unsettled markets. The subsequent 60-day ceasefire reopening the Strait of Hormuz in mid-June, combined with Fitch’s sovereign upgrade to BB (South Africa’s first ratings upgrade in some 21 years), then drove a sharp compression in SA bond yields. The FTSE/JSE All Bond Index returned close to 7.9% for the quarter — one of its strongest quarters in years.

This bond rally flowed directly through to the income-orientated managers. The Nedgroup Inv Flexible Income Fund returned 3.20% for the quarter — its floating rate structuring again proved well-suited to a volatile rate environment. PortfolioMetrix Dynamic Income and Granate’s income strategy similarly posted strong absolute numbers, though several lagged the raw bond index given more conservative duration and credit positioning.

Local equity managers had a tougher quarter. All our incumbent managers posted negative quarterly returns, driven by a sharp correction in gold and platinum group metal prices — gold fell from January’s high just over $5,400/oz to around $4,000/oz by late June, as hawkish Fed repricing removed the safe-haven bid. This dragged the broader market lower too: the FTSE/JSE All Share Index fell for a second consecutive month in June (-3.7% for the month alone), taking its first-half 2026 return to -3.0%. Fairtree, with its larger precious metals exposure, was hit hardest (-6.66% for the quarter). Truffle was the most defensive, holding a significantly lower weight to precious metals while carrying a larger exposure to bank stocks that enjoyed a strong quarter. The rally in banking shares was driven primarily by strong bank earnings, a firming rand, falling energy prices that compressed bond yields, and improving global risk appetite following the US/Iran ceasefire.

Year-to-date to 30 June, three of the four funds have now recovered to positive territory — Balanced Plus re-mains marginally negative at -0.61%, Balanced sits at +0.40%, Income Provider at +1.87%, and Defensive Income leads at +3.73%.

As we move into the second half of 2026, we continue to monitor the durability of the Hormuz ceasefire, the SARB’s next decision on 23 July, and the Fed’s rate path under its new leadership — all of which remain live sources of volatility for both bonds and precious metals. We will continue to look for opportunities as they present themselves, while remaining prudent and avoiding reactive shifts in the absence of greater certainty.

Note: Quarterly performance since inception: Platinum BCI Balanced fund of Funds and Balanced Plus Fund of Funds: Annualised return is weighted average compound growth rate over the period measured. Actual annual figures are available to the investor on request. Source Morningstar as at 30.06.2026.

Note: Quarterly performance since inception: Annualised return is weighted average compound growth rate over the period measured. Actual annual figures are available to the investor on request. Source Morningstar as at 30 June 2026.

Platinum Global Managed Fund

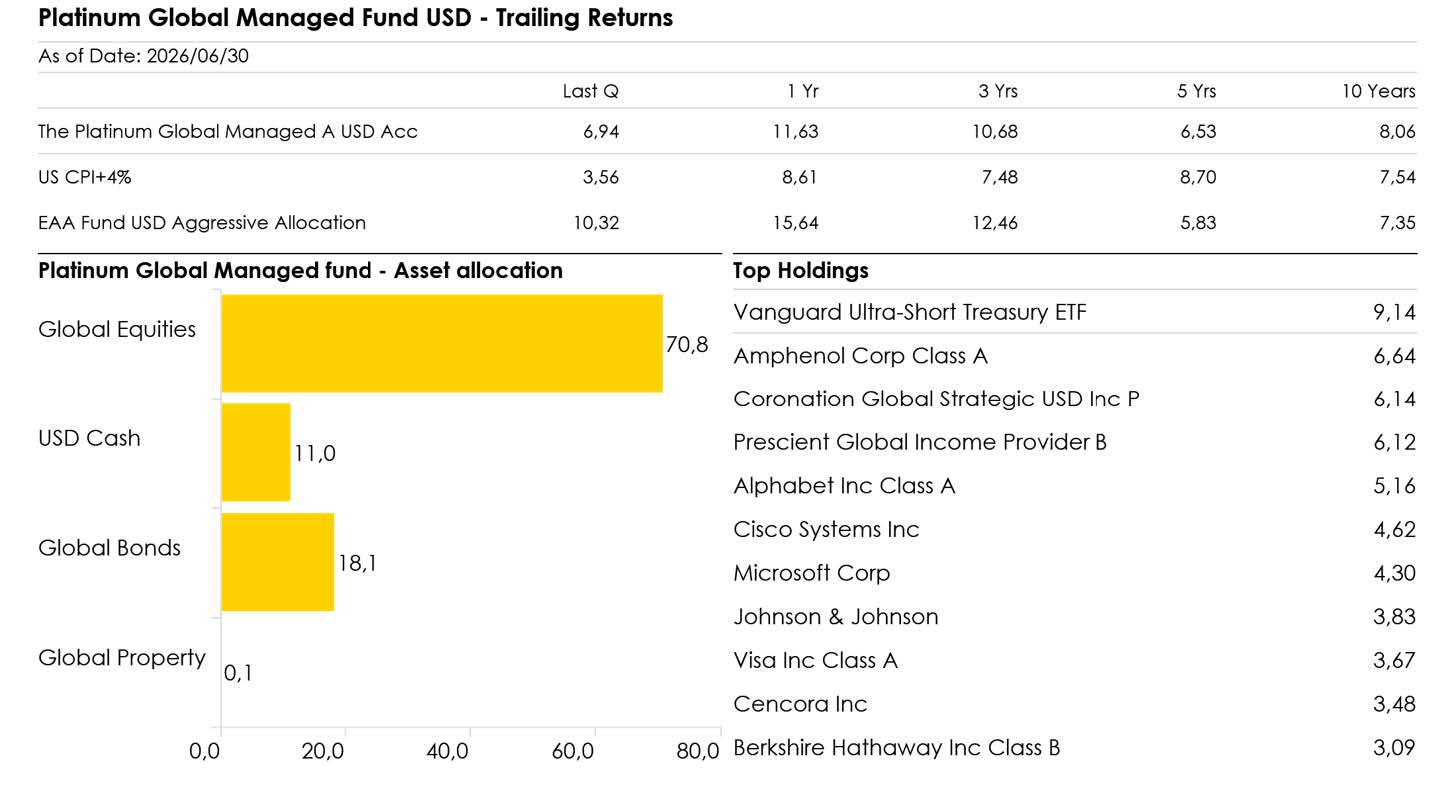

The Platinum Global Managed Fund delivered a strong performance during the second quarter of 2026, comfortably outperforming its benchmark of US CPI +4%. While we are pleased with this outcome, the recent increase in US inflation means that the benchmark itself is rising, making it a more demanding target to outperform over the coming quarters.

The portfolio ended the quarter with an equity allocation of just under 71%, with the balance invested in cash, short-dated debt instruments and ultra-short-dated US Treasuries. This positioning provides liquidity and flexibility while allowing us to remain invested in high-quality businesses that we believe are well positioned to compound shareholder value over the long term. During the quarter, the US dollar also strengthened, providing a modest tailwind to returns.

Following the portfolio rebalancing at the end of the first quarter, we made no changes to the portfolio during the second quarter. We remain comfortable with our holdings and continue to believe that they represent exceptional businesses with durable competitive advantages, strong balance sheets and proven management teams.

The first-quarter earnings season reinforced this conviction. The majority of the companies in our portfolio met or exceeded market expectations, with particularly strong results from our technology, healthcare, financial and consumer holdings. While some companies continue to face cyclical headwinds or are investing heavily for future growth, we saw no evidence of any material deterioration in the underlying quality of the businesses we own.

Performance during the quarter was led by Amphenol, Cisco Systems and Alphabet. Amphenol continued to benefit from strong demand for AI infrastructure and high-speed connectivity solutions, while Cisco delivered another solid quarter as investment in AI networking and data centre infrastructure gathered momentum. Alphabet reported excellent earnings, with continued strength in Search and Cloud and growing evidence that its significant AI investments are beginning to translate into improved business performance.

The main detractors from performance were Zoetis and Cencora. Zoetis came under pressure as investors remained cautious about the normalisation of spending in the companion animal market, despite the company’s strong long-term fundamentals. Cencora also lagged during the quarter, although this reflected relative market rotation rather than any deterioration in the business. The company continues to generate resilient earnings and strong cash flows, reinforcing our confidence in its long-term investment case.

Periods of market uncertainty often reinforce the importance of owning high-quality companies. Businesses with strong competitive advantages, resilient earnings, high returns on capital and disciplined capital allocation are typically better positioned to navigate changing economic conditions and continue creating long-term shareholder value. We believe this quality bias remains one of the key strengths of the Platinum Global Managed Fund and will continue to underpin our investment approach.

Note: Quarterly performance since inception: Highest: 16.11% Lowest: -8.98%. Annualised return is weighted average compound growth rate over the period measured. All performance figures quoted are sourced from Morningstar. Period ending 30 June 2026.

Stock in Focus: Motorola Solutions

Mention Motorola and most people picture a mobile phone. The RAZR flip phone, perhaps, or the brick-sized handset from the 1980s. What very few realise is that the Motorola that makes phones and the Motorola we own in the portfolio are no longer the same company. In January 2011, the original Motorola split in two. The consumer side, Motorola Mobility, took the phones and was sold to Google the following year for roughly $12.5 billion, before eventually being passed on to Lenovo. The other half, Motorola Solutions, kept the decidedly less glamorous business of two-way radios and public safety communications. At the time, it looked like the boring leftover. In hindsight, the boring leftover was the crown jewel.

Since that split, Motorola Solutions has quietly become embedded in the fabric of everyday life in a way almost no one notices. When you dial an emergency number, when a police officer speaks into a shoulder radio, when a fire crew is dispatched to a burning building, when a body camera records an incident, or when a city control room coordinates a response, there is a very good chance Motorola Solutions technology is somewhere in that chain. It is one of those rare businesses that touches millions of lives daily while remaining almost invisible to the public. That invisibility is precisely what makes it interesting.

A Business Built on Mission-Critical Trust

At its core, Motorola Solutions builds the communication and security backbone that public safety agencies and governments depend on. Its land mobile radios, the rugged two-way devices used by police, fire and emergency services, remain the gold standard, and the company has pioneered police radio since 1930. In the United States it is the clear market leader in public safety communications.

This is not an accident. Agencies build entire networks around Motorola’s systems, train their people on them, and rely on them in life-or-death situations. Once that infrastructure is in place, it is enormously difficult and risky to rip out and replace. That creates exactly the kind of durable competitive moat and high switching costs we look for in a long-term holding.

That leadership has been built over nearly a century of working alongside the public safety agencies it serves, and today it designs technology for more than 100,000 customers across over 100 countries. When the product you sell is the thing a first responder trusts with their life, reliability and reputation matter more than price, and that is a very comfortable position for a business to occupy.

From Hardware to Recurring Software

What makes Motorola Solutions more than just a radio company is the way it has evolved. The business is now managed in two halves. The first, Products and Systems Integration, houses the traditional radio and video security hardware. The second, Software and Services, is where the more exciting story sits. This segment, which includes command centre software, video security, and managed services, now accounts for roughly 38% of sales and is growing considerably faster than the hardware side. In 2025, Software and Services grew 13% while the products segment grew 5%, with command centre software in particular growing at 19% in the final quarter.

This shift matters because software and services revenue tend to be recurring and subscription-based, making it more predictable and higher quality than one-off equipment sales. Motorola is steadily embedding artificial intelligence across this portfolio, from tools that help 911 call-takers manage overwhelming call volumes to systems that turn hours of radio traffic, video and audio into usable intelligence for investigators. The company ended its most recent quarter with a record backlog of around $15.7 billion, which gives us strong visibility into future revenue, another quality we prize.

Moving Into Drones: Promising, But Still Early

The newest chapter, and the one generating headlines, is Motorola’s push into the rapidly growing ecosystem around drones and unmanned systems. In August 2025 it completed the $4.4 billion acquisition of Silvus Technologies, a leader in mobile ad-hoc network technology that allows secure video, voice and data to move between devices without fixed infrastructure. It is the kind of resilient, self-healing communications network that is increasingly critical to drones, autonomous systems and defence applications. This extends Motorola into what it describes as a multi-billion-dollar, rapidly growing market, and fits neatly with its ‘drone as first responder’ ambitions, where aerial units are dispatched to give responders eyes on a scene before they arrive.

We think this is genuinely exciting, but we want to be clear-eyed about it. Silvus only closed in the second half of 2025 and contributed a relatively small amount of revenue against Motorola’s $11.7 billion total. Integrating a $4.4 billion acquisition is a substantial undertaking, and the drone opportunity is still in its early innings. For now, we view it as promising optionality rather than a proven growth engine, an additional way to win layered on top of an already profitable core.

Why We Own It

We like businesses with durable moats, mission-critical products, and multiple paths to grow. Motorola Solutions ticks all three. It dominates a market where trust and reliability matter more than price, it is steadily shifting towards higher-quality recurring software revenue, and it now has a credible new avenue in drones and unmanned systems. Add to that a record backlog, strong cash generation, expanding margins, and nearly a hundred years of accumulated relationships, and you have a business that is far more resilient than its dull public image suggests.

Investors often chase the newest technology, but sometimes the best businesses are the ones quietly solving essential problems that few people ever notice. That is exactly the kind of quiet, durable compounder we are happy to own in our portfolios.