Global Market commentary and 2025 Outlook

The markets

U.S. stocks delivered another blockbuster performance in 2024. The S&P 500 soared 24%, marking its strongest gain since 2019, as the economy demonstrated remarkable resilience and inflation pressures eased. Technology stocks were a driving force behind the rally, propelling the index to its best twoyear streak since 1997 and 1998, according to Dow Jones Market Data.

The market rally has created new wealth and heightened investor optimism. The December Bank of America Global Fund Manager Survey revealed a fiveyear high in enthusiasm for U.S. stocks. Other asset classes also delivered notable returns, with gold poised for its best year since 2010 and bitcoin surpassing $100,000 before retreating slightly below that mark.

The economy

The U.S. economy displayed impressive strength in 2024, with resilient consumer spending supporting a fourth consecutive year of abovetrend growth. Looking ahead to 2025, policy uncertainty clouds the economic outlook, though no major threats to shortterm growth have emerged. A continuation of trendlike growth is expected, underpinned by steady consumer activity and supportive fiscal policies.

The labour market stabilised after an initial rise in unemployment in early 2024. In 2025, steady growth should sustain job creation, limiting the risk of significant unemployment increases. Wage growth is also expected to stabilise, supported by productivity gains. This dynamic should help inflation continue its descent toward the Federal Reserve’s 2% target.

Earnings growth exceeded expectations in 2024 and is forecast to accelerate further in 2025. Challenges such as slowing nominal growth and easing inflation could pressure revenues and margins. However, broader earnings participation and favourable fiscal policies should reduce risks associated with elevated concentration and valuations, creating more opportunities for active investors.

Inflation made progress toward the 2% target in 2024, enabling the Federal Reserve to reduce rates by 100 basis points. While the pace of disinflation slowed late in the year, this was largely due to base effects, with no significant evidence of rising price pressures. In 2025, inflation is expected to continue its downward trajectory as prices for shelter and auto insurance normalise. However, potential inflationary policies, such as tariff adjustments, could pose challenges to this outlook.

Geopolitical and Policy Dynamics

Geopolitical tensions and supply chain disruptions have prompted a reevaluation of global trade policies. Proposed aggressive tariffs under the incoming administration of Presidentelect Trump could lead to higher inflation and retaliatory actions from trading partners, exacerbating uncertainty. While these changes may create headwinds, they could also unlock opportunities in sectors resilient to inflation.

Labor market dynamics also present a mixed picture. While the U.S. labour supply has recovered impressively due to strong immigration, severely curtailed immigration policies could slow growth and exert upward pressure on wages, potentially fuelling stagflation.

The Federal Reserve’s cautious approach to monetary easing is likely to continue into 2025, with gradual rate cuts contingent on economic data. Resilient activity and potential inflationary policies could temper the pace of easing, maintaining a relatively neutral stance on interest rates.

Outlook for 2025

The U.S. economy is wellpositioned for another year of solid growth. Enhanced productivity, particularly in the technology sector, is expected to support this momentum. Fiscal policies under the new administration aim to stimulate domestic investment, potentially revitalizing key industries and driving job creation. While tariff adjustments may introduce inflationary pressures, they also open avenues for strategic investments in sectors that can withstand these challenges.

Corporate resilience will remain a defining feature of the U.S. market in 2025. Earnings growth is projected to stay robust, with the technology and healthcare sectors leading the charge. The rapidly growing AI industry continues to diversify, offering compelling opportunities across financial services, manufacturing, and other sectors. Despite concerns about overvaluation in certain areas, undervalued companies could present attractive prospects for discerning investors.

With liquidity at just under 30% in our Global Fund and ample reserves across our other portfolios, we are poised to deploy capital strategically during potential market pullbacks. This ensures that our investors can capitalize on evolving market conditions. The Federal Reserve’s balanced monetary policy approach further supports our constructive outlook, fostering an environment conducive to equity growth even amid mild inflationary pressures.

Conclusion

As we transition into 2025, the U.S. economy and markets appear set to navigate a year of measured growth and evolving opportunities. Active management, supported by thoughtful capital allocation and a keen focus on emerging trends, will be critical to capturing value in this dynamic landscape. We remain committed to delivering strong outcomes for our investors by staying agile and responsive to changing conditions.

Fourth Quarter 2024 Local Market Commentary

The Johannesburg Stock Exchange (JSE) ended 2024 with a 13% gain, but the last quarter was tough due to lots of ups and downs. This was largely because of things happening around the world, especially the U.S. election where Trump got reelected, leading to new policies like high tariffs on Chinese goods, which shook up global markets.

The South African rand weakened, moving from 17.12 to 18.87 against the dollar. This was bad news for South Africa since China is a big trade partner and our economy depends a lot on commodity prices, which fell with China’s slowdown. South African resource stocks dropped by nearly 10% in Q4.

Locally, South Africa’s economy shrank by 0.3% in the last quarter, lower than expected because of ongoing problems like issues with Transnet. Confidence among businesses and consumers was low, and despite better electricity management by Eskom, economic recovery was weak.

Outlook for 2025

Looking ahead to 2025, how South Africa’s stock and bond markets do will depend on things like inflation, GDP growth, and jobs, as well as how the U.S. and China get along. New U.S. policies could make trade tougher, affecting South Africa’s economy and the rand’s value.

The South African Reserve Bank will probably follow the U.S. Federal Reserve’s lead on interest rates to keep the rand from falling further. This might mean less aggressive rate cuts even if our economy needs them.

The success of the new Government of National Unity in fixing problems in energy, logistics, and crime will be crucial. If they succeed, it could boost local investments, but for now, being careful with South African stocks might be wise. Global trade tensions between the U.S. and China will also play a big role, so investors need to watch both local reforms and international news closely.

Insights

Seeing More, Waiting Longer: A Path to Better Decision-Making

In today’s fast-paced world, immediacy and spontaneity dominate. Every external pressure pushes us to act quickly, to react rather than reflect. Yet, in both art and investment management, it is not speed but patience that unlocks true insight and value. This is a lesson we can learn from David Hockney’s exploration of perception and the deliberate act of spending time with John Singleton Copley’s Boy with a Squirrel.

Vision Isn’t Immediate; Nor Is Understanding It is tempting to think that seeing and by extension, decision-making is instantaneous. But as both Hockney’s work and the experience of looking at Copley’s painting illustrate; vision is a process. What appears simple and straightforward at first glance can contain depths of complexity and connections that only reveal themselves with sustained attention.

For example, in the Copley exercise, the act of spending three hours looking at a single painting unlocks details and relationships invisible at first. These details the echo of the boy’s ear in the squirrel’s ruff, the alignment of the chain and water glass—only emerge through time. Similarly, Hockney’s art challenges us to “see more,” encouraging us to look beyond surface appearances and traditional perspectives. His work reminds us that perception is layered, dynamic, and often slow.

This principle applies directly to us at Platinum Portfolios. It is easy to assume that access to information equates to understanding. It’s just the starting point. Turning information into actionable knowledge requires patience, critical attention, and time.

Time as a Formative Force – good investment decision take time. Companies, like paintings, are rich with layers of data, history, and nuance. To truly understand a company’s value or potential requires more than a quick glance at earnings reports or market trends it demands patient investigation and a willingness to delay judgment.

This delay isn’t a weakness; it’s a strength. Details that initially seem insignificant in a company’s financials and business strategy may reveal critical insights when viewed over time.

Productive Delays: Patience as a Skill Hockney’s philosophy and the Copley exercise both teach us that delay is not a passive intermission but an active and productive force. Deliberate delays allow for deeper analysis, the uncovering of hidden patterns, and more informed decision-making. In the context of fund management, this means resisting the urge to act on surface appearances or shortterm market fluctuations. Instead, it means taking the time to see the full picture, to understand not just the immediate opportunities but the deeper structural realities.

This kind of patience is a skill, a form of time management that is increasingly rare in our world of instant communication. But it is a skill that must be cultivated at Platinum Portfolios to make better decisions for our clients to generate good returns. Patience transforms disempowerment into power; it turns waiting into a productive cognitive state.

In the thousands of years before instant communication, human understanding was built on delay, on the slow, deliberate process of making and observing. To be good fund managers, we must reclaim this formative value of time. By learning to see more, through patience and critical attention, we not only become better fund managers but also better thinkers, capable of unlocking better wealth and returns for our clients.

Report back on our funds

The Platinum BCI Worldwide Flexible Fund

The Platinum BCI Worldwide Flexible Fund had a strong quarter, delivering a solid return of 5.61%. Over the past three years and longer, the fund has remained one of the top performers in its category. As we approach the end of 2024, the fund has achieved a 10.52% return for the year and is well-positioned as we enter 2025.

Market Overview: Global markets faced challenges in the fourth quarter of 2024, with the FTSE-JSE Capped SWIX Index dropping by 2.1%. Factors like the prospect of higher U.S. interest rates, a stronger U.S. dollar, and weaker global equity sentiment contributed to this decline. However, South African bonds performed exceptionally well, delivering a robust 17.18% return for the year.

Key Contributors and Detractors: Among our best-performing stocks this quarter were Visa, Williams-Sonoma, and Walmart. On the other hand, BHP, Zoetis, and Amgen underperformed. Over the year, Williams-Sonoma, Visa, and Berkshire Hathaway led the way, while Nike, BHP, and Comcast detracted from returns.

We made some strategic decisions during the year: We sold our holdings in British American Tobacco. We made a decision to sell Comcast, as changes in its business environment and rising debt made it a less attractive investment. We added to our position in Nike, buying at lower levels. We believe in Nike’s long-term growth potential, driven by innovation and expansion plans.

Portfolio Strategy: Locally, the fund has 14% exposure to South African fixed-income assets. With the South African Reserve Bank maintaining a hawkish stance, we see opportunities to capture strong real yields and plan to extend the duration of our bond holdings. Globally, the fund balances liquidity with investments in both short- and long-term bonds. Offshore short-dated bonds are offering attractive yields, providing flexibility for future opportunities.

Outlook: We are cautiously optimistic about local market returns in 2025 and remain confident in the prospects of the companies in our portfolio. In the U.S., we believe economic resilience will continue to support businesses, and our focus on strong companies with solid fundamentals remains unchanged. These companies have robust finances, recognisable brands, competitive advantages, steady cash flows, and low debt levels, qualities that help them perform well even in challenging economic conditions.

Looking ahead, we are tracking additional companies that align with our investment criteria. These stocks are slightly above our target buy price, and we hope to add them to the portfolio if valuations become more favourable. We are committed to working diligently to deliver strong returns for our investors. Thank you for your trust in us, and we look forward to a successful 2025.

Note: Quarterly performance since inception: Highest 13.17% Lowest -6.68%. Annualised return is weighted average compound growth rate over the period measured. Actual annual figures are available to the investor on request. Source Morningstar as at 31 December 2024.

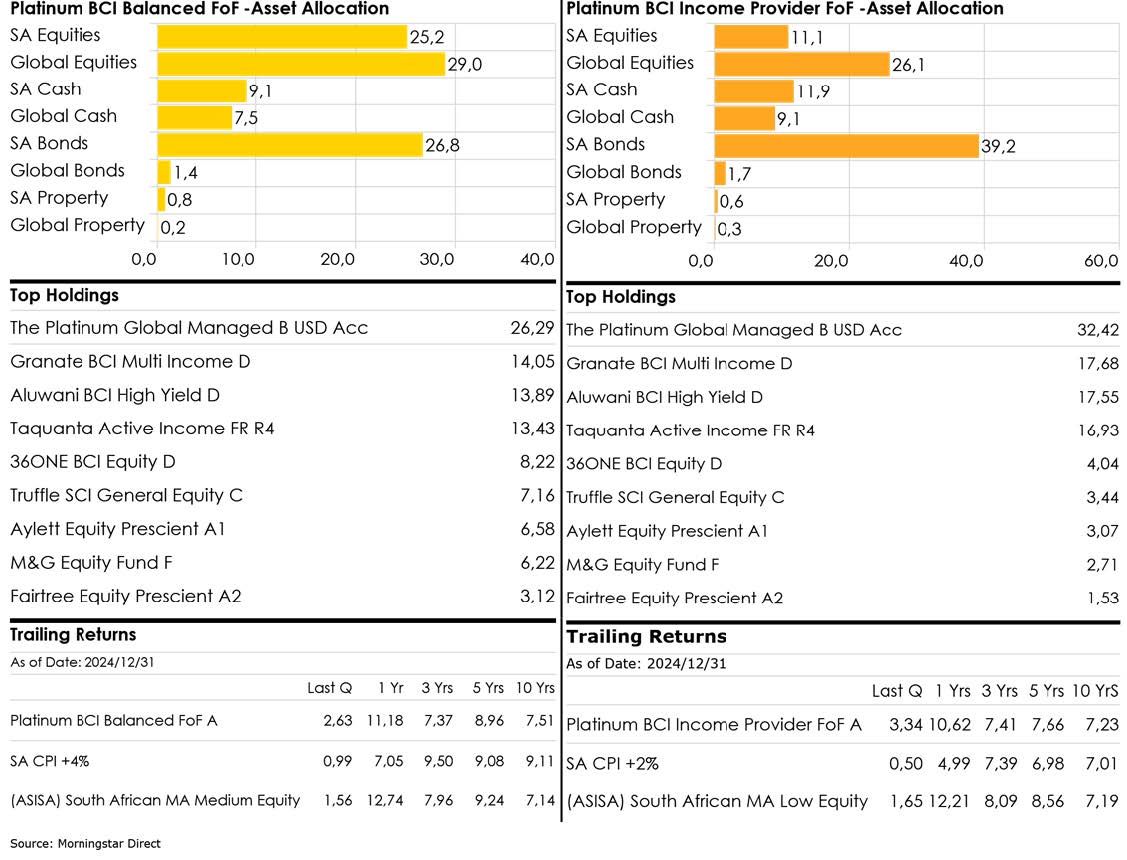

The Platinum BCI Balanced Fund of Funds and the Platinum BCI Income Provider Fund of Funds

The year 2024 was notably successful for investors in the Balanced Fund and Income Provider Funds, which delivered robust real returns. The Balanced Fund achieved a return of 11.18%, comfortably surpassing its CPI+4% benchmark of 7.05%. Similarly, the Income Provider Fund returned 10.62%, outperforming its CPI+2% benchmark by a margin, which stood at 4.99%. These performances underscore the strategic asset allocation and investment decisions made throughout the year.

Our investment approach for 2024 was characterised by a bearish outlook on the South African economy, leading us to favour offshore investments in hard currencies and maintain a short duration on local bonds. This strategy paid off in the first half of the year, as global markets were cautious due to uncertainties surrounding South African elections and global inflation trends. During this period, both funds performed admirably, not only meeting but exceeding their respective benchmarks and peer group averages.

Our investment approach for 2024 was characterised by a bearish outlook on the South African economy, leading us to favour offshore investments in hard currencies and maintain a short duration on local bonds. This strategy paid off in the first half of the year, as global markets were cautious due to uncertainties surrounding South African elections and global inflation trends. During this period, both funds performed admirably, not only meeting but exceeding their respective benchmarks and peer group averages.

However, the landscape shifted in the second half of the year with the establishment of the Government of National Unity (GNU) in South Africa and signs of decreasing inflation both domestically and in the U.S. This led to a significant rally in local equity and bond markets. The yield on South Africa’s 10-year government bond dropped from a peak of 10.90% to 8.80%, and the rand appreciated by over 10%. While our funds still managed to outperform their inflation-adjusted targets, they lagged behind some peers who might have capitalised more aggressively on these local market upturns.

Throughout the year, we continuously monitored, analysed, and debated our fund allocations. We reaffirmed our belief in the relative strength of the U.S. economy compared to South Africa’s, despite the optimism surrounding the GNU’s formation. We resisted the temptation to be swept up in the euphoria of the peaceful political transition in South Africa and instead chose to bolster our offshore exposure by investing in a Vanguard ETF focusing on U.S. equities.

The last quarter of 2024 brought about a reversal in market dynamics. The rand weakened significantly, moving to around 19 against the dollar, and local bond yields climbed back above 9.15%. Concurrently, U.S. equities continued their strong performance, outpacing local equities by 14% when measured in rand terms. This scenario allowed our funds to not only outperform their benchmarks but also to surpass many of their peers in this final quarter of the year.

Looking forward, we maintain a cautiously bullish stance on equities as an asset class, with a particular inclination towards global equities over local. We believe that the “Trump Trade” – a term referring to market movements influenced by U.S. policy under Trump’s administration – still has some momentum left in the U.S. markets. Despite the high valuations of the S&P 500, our deep understanding of the intrinsic valuations of the global stocks within our investment solutions gives us confidence in our current allocations and potential upside.

We are mindful of the risks associated with high valuations and geopolitical tensions but remain committed to our strategy of seeking quality global investments while keeping a cautious eye on South Africa’s economic and political developments. This approach not only aims to protect capital but also to provide growth opportunities in a global context where the U.S. market, in particular, continues to offer promising prospects due to its economic resilience and policy environment.

Note: Quarterly performance since inception: Platinum BCI Balanced fund: Highest 8.62% Lowest -3.90%. Platinum BCI Income Provider fund: Highest 5.28% Lowest -1.84%. Annualised return is weighted average compound growth rate over the period measured. Actual annual figures are available to the investor on request. Source Morningstar as at 31 December 2024.

Platinum BCI Defensive Income Fund of Funds

The Defensive Income FoF provided investors with 2.54% returns over the quarter, and 10.46% for the year. This was in line with its cash+2% benchmark.

The main drivers of performance were from local inflation-linked bonds and the underlying credit exposure as local credits spread contracted over the quarter. A small exposure to foreign property detracted from the overall performance, mainly due to postponed expectations for the next Federal Reserve rate cut, now anticipated in June 2025.

The fourth quarter of 2024 was volatile for South African bonds, which saw the 10-year government bond yield peaking at 9.51% before settling slightly above 9% by year-end. This volatility resulted in a modest return of 0.43% for the FTSE/JSE All Bond Index. Despite such market conditions, our underlying fund managers adeptly navigated this environment, achieving strong returns for the fund.

Interest rates in South Africa are not expected to decrease as initially forecast. This shift is largely influenced by persistent core inflation in the US, which could pressure the South African Reserve Bank to maintain higher rates longer than expected. Additionally, a potential weakening of the rand adds another layer of complexity to the interest rate dynamics. Given these circumstances, holding bonds at the lower end of the yield curve becomes increasingly advantageous. Low-duration bonds are less sensitive to interest rate fluctuations, thereby reducing price risk while still offering an attractive yield, currently hovering around 10%. This approach not only helps in mitigating potential losses from rising rates but also ensures a steady income stream for investors.

The Platinum Global Managed Fund USD

Market Overview: The fourth quarter of 2024 was characterized by volatility as global stocks faced pressure from investor concerns about economic growth and persistent inflation. The Federal Reserve adjusted its outlook, reducing its forecast to just two rate cuts in 2025. Meanwhile, Donald Trump’s presidential victory and the anticipation of additional tax cuts and expansionary fiscal policies provided support for U.S. equities. However, outside the United States, investor sentiment was weighed down by concerns over the president-elect’s proposed tariff policies and their potential impact on global trade. Against this backdrop, the MSCI World USD Index declined by -0.67% for the quarter, while the Platinum Global Managed Fund USD ended the period down -1.70%.

Key Drivers of Performance: The fund’s performance was supported by strong contributions from select holdings, including Williams-Sonoma, Visa, Walmart, Cisco, and Apple. However, our overall underperformance for the quarter was primarily attributed to challenges in the pharmaceutical sector. Positions in Zoetis, Amgen, Johnson & Johnson, and Nike were the main detractors during this period.

Portfolio Adjustments: During the quarter, we made one key adjustment, trimming our position in Walmart. The company’s strong share price performance led it to reach our pre-determined sell price, prompting us to lock in gains. We remain optimistic that market drawdowns will present opportunities to add high-quality companies currently on our watchlist to the portfolio.

Managing Risk in Volatile Markets: We maintain a stance of cautious optimism while recognising that market volatility is likely to persist. Our strategy remains unchanged: we will continue to hold our current asset allocation while maintaining a cash buffer to mitigate volatility and downside risks. Our confidence in our portfolio holdings is underpinned by a focus on high-quality, resilient businesses that have historically demonstrated the ability to navigate challenging market conditions while delivering strong long-term returns.

Looking Ahead: As we move into 2025, we remain confident in the fund’s positioning, which strikes a balance between growth and prudent risk management. Our portfolio is composed of robust companies with strong fundamentals, and our disciplined investment approach ensures we remain well-positioned to capitalise on long-term opportunities. We are committed to delivering the solid long-term performance that our investors have come to expect.

Thank you for your continued trust and investment in the Platinum Global Managed Fund.

Note: Quarterly performance since inception: Highest: 16.11% Lowest: -8.98%. Annualised return is weighted average compound growth rate over the period measured. All performance figures quoted are sourced from Morningstar. Period ending 31 December 2024. Actual annual figures are available to the investor on request.

Stock in Focus: Walmart

Walmart is one of the world’s largest retailers, with 10,500 stores across nineteen countries. Known for its “Everyday Low Prices” promise, Walmart serves a wide range of customers by offering everything from groceries and electronics to clothing and household essentials. Over its 60-year history, the company has continuously adapted to remain a dominant force in retail.

Walmart’s Recent Success

In recent years, Walmart has made significant changes to its business model, setting itself apart from competitors. One of its biggest achievements has been attracting higher-income customers. By modernising stores and introducing premium products like Apple devices and Bose headphones, Walmart expanded its appeal beyond budget-conscious shoppers. This shift was a key driver of U.S. market share gains, with higher-income households accounting for 75% of this growth.

Beyond attracting wealthier consumers, Walmart has diversified its revenue by investing in high-margin areas such as advertising and memberships. The Walmart Connect advertising platform and international ventures like Flipkart have significantly boosted ad revenue. Additionally, membership services like Walmart+ and Sam’s Club have seen robust growth, further enhancing the company’s profitability. Walmart’s online sales have also surged, thanks to investments in seamless pickup and delivery services and improvements to its online marketplace. Automation has played a crucial role, with over half of its fulfilment centres now using advanced technology to improve efficiency and scale operations.

The Role of Technology

Technology has been at the heart of Walmart’s transformation. The company uses data analytics to optimize inventory management, ensuring that products are available when and where customers need them. Artificial intelligence (AI) helps forecast demand, reducing waste, and improving supply chain efficiency. Walmart has also integrated automation and robotics to speed up order fulfilment while cutting costs. These advancements not only enhance operations but also improve the customer experience by ensuring faster and more accurate deliveries.

Pricing and Market Position

Despite inflationary pressures, Walmart has reinforced its reputation for affordability by strategically rolling back prices on thousands of items. This approach has attracted cost-conscious shoppers while also expanding its reach across all income groups. As a result, Walmart delivered an outstanding performance in 2024, with its share price surging more than 80%. This growth highlights the company’s resilience and ability to thrive despite economic challenges.

Looking Ahead

Walmart has a clear roadmap for future growth. The company is investing heavily in AI-driven inventory management and personalised customer experiences to further enhance its digital capabilities. It is also exploring opportunities in high-growth international markets, particularly in Southeast Asia and Latin America, through partnerships and acquisitions like Flipkart.

In addition, Walmart is expanding in high-margin sectors such as advertising, memberships, and healthcare services. Its Walmart Health initiative aims to provide affordable medical care to a broader audience. Sustainability remains a core focus, with ongoing efforts to reduce environmental impact and improve social responsibility.

Why We Like Walmart

Walmart’s ability to attract new customers, diversify its revenue streams, and embrace digital transformation has fuelled strong financial performance. We are particularly excited about its focus on technological innovation, margin expansion, and global growth. Given its proven track record and strategic vision, we believe Walmart is well-positioned to continue delivering long-term value to investors.